Debt Recycling: The Tax ‘Scam’ Your Banker Doesn't Want You to Know About (It's Legal)

See how much you could benefit using debt recycling with our debt recycling calculator

See how much you could benefit using debt recycling with our debt recycling calculator

Why Bother With Debt Recycling?

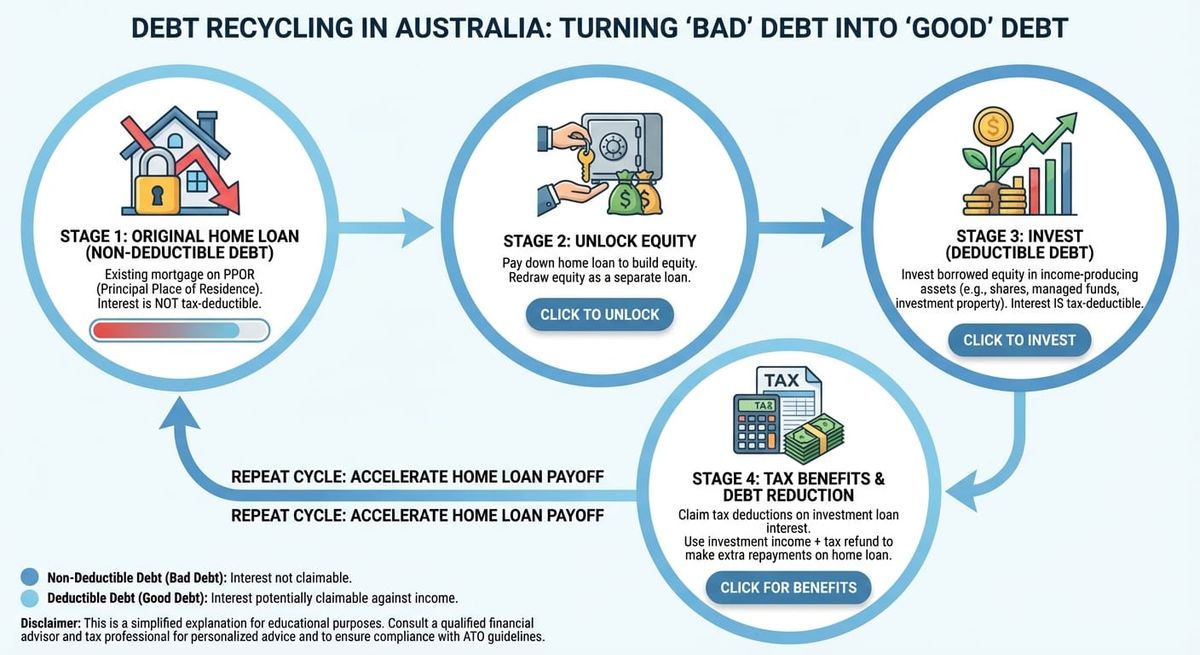

Stop paying full tax on your investments!. Seriously, at its core, it's just a 100% legal way to flip your debt from the "Bad" column (non-deductible home loan) to the "Good" column (deductible investment loan). You get to write off your debt interest against your income. It's debt restructuring 101, and it's gold.

The formula for the saving is simple—it’s just how much tax you avoid:

Example:

6% x $1,000,000 x 37%

= $22,200 (Tax Saved)

When Does This Tax Strategy REALLY Pay Off?

Look at the formula above. The variables that juice your return are a higher interest rate, a higher marginal tax rate (i.e., you earn more), or a bigger investment. Hot Tip: Don't switch to a crap home loan just to chase a high rate. The point is, when rates are rising, the amount you can claim on your tax return goes up with it. That’s a win.

Got a Mortgage AND Spare Cash to Invest? Should you bother?

Yes. This is the only scenario where this magic trick works. If you have non-deductible debt (your home loan) and you have cash waiting to be invested in an income-producing asset (shares/property), you're the target audience.

What if I want to keep my spare cash in my offset or redraw?

Nope. Hard pass. You need to actually use the money to buy an asset that makes income. Keeping it in your offset or redraw is just cash. The ATO doesn't care about your cash savings—they care about how you’ve used the debt.

What if the interest earned on shares is less than the interest cost of the loan (A.K.A. Negative Gearing)

That's just called negative gearing, and while we love a good tax write-off, that is not debt recycling. Debt recycling is specifically about shifting your non-deductible home loan debt into deductible investment debt to smash your tax bill.

So, What's the Real Competition to Debt Recycling?

You only compare Debt Recycling to one thing: taking your spare cash and investing it directly into shares while keeping your original home loan debt untouched. DO NOT compare it to just holding cash in your offset/redraw. That’s a false comparison, because cash is low-risk, and shares are high-risk. It’s apples to bananas—stop it.

When Should You Walk Away From Debt Recycling?

If you fit into any of these categories, forget about it:

- You pay zero tax (congrats, but no tax to save).

- You don't have spare cash to invest.

- You don't have a home loan (no non-deductible debt to flip).